The $100,000 Question Every High School Senior Should Ask

What a portfolio manager told my students about college debt, compound interest, and the financial advantage young people don’t realize they have.

ESSAY CURE’s Christine Gacharná sits down with Todd O. Pettibon, Partner at Toth Financial, to discuss the Return on Investment (ROI) of a college degree that students should consider.

If you’re 18 years old, someone is about to ask you to make a $100,000 decision.

And most people will tell you to make it in about five minutes.

The decision is college.

For decades, the advice has been simple:

“Go to college.”

But that advice leaves out an important detail.

College is not just an educational decision.

It’s one of the largest financial investments most families will make, behind saving for retirement and buying a home.

I sat down with a portfolio manager to talk about this exact issue with high school students. What started as a conversation about college quickly turned into something much bigger:

How money actually grows over time — and why the decisions students make in their early twenties matter more than they may think.

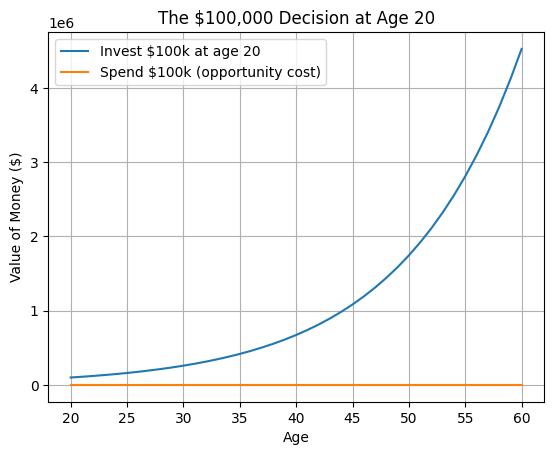

The $100,000 Decision

If $100,000 is invested at age 20 and earns an average 10% annual return, it could grow to more than $4 million by age 60. This illustrates the opportunity cost of large financial decisions early in life.

This doesn’t mean students shouldn’t go to college. It means they should think carefully about how much they spend to do it. Reducing the cost of college by even $20,000–$40,000 can dramatically change long-term financial outcomes.

The Hidden Price Tag of a Bachelor’s Degree

Let’s start with the numbers.

The average in-state tuition for a four-year degree is about:

$45,000 for tuition, books, and fees.

Add room and board, and the real cost climbs closer to:

$80,000–$100,000.

That’s a staggering amount of money for someone just beginning adulthood.

And like any investment, it raises a simple question:

What do you get in return?

On average, the answer is: quite a lot.

According to Social Security data, people with a bachelor’s degree earn significantly more over their lifetime than those with only a high school diploma.

Rough estimates suggest:

Men with a bachelor’s degree earn about $900,000 more over their lifetime

Women earn about $630,000 more

Graduate degrees increase that gap even further.

But there’s a catch.

You only get the return if you actually graduate.

Many students take on tens of thousands of dollars in loans —

and never finish their degree.

Which means they carry the debt without receiving the benefit.

The Financial Concept Every Student Should Know

During our conversation, Mr. Pettibon explained something called the Rule of 72.

It’s one of the simplest ways to understand how investing works.

The rule is straightforward:

72 ÷ your rate of return = how many years it takes your money to double.

If your investments grow at 10% per year, your money doubles roughly every 7.2 years.

That means if you invested $86,000 at age 20, here’s what could happen:

Age 20 → $86,000

Age 27 → $172,000

Age 34 → $344,000

Age 41 → $688,000

And that’s without adding a single additional dollar.

That’s the power of compound interest.

Your money starts making money —

and then that money starts making money, too.

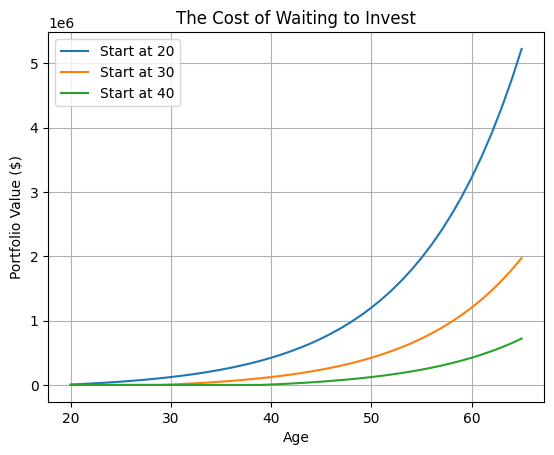

What the chart demonstrates

By age 65:

Start at 20 → ~$5.2 million

Start at 30 → ~$2.0 million

Start at 40 → ~$740,000

Even though the monthly investment is the same, the person who starts at 20 ends up with more than double the wealth of someone who starts at 30.

This is the time value of money + compounding.

The Most Important Financial Advantage Young People Have

Young people often assume their biggest financial advantage will be:

getting a high salary

choosing the right career

working harder than everyone else

But none of those are actually the biggest advantage.

The real advantage is time.

Time is what allows compound interest to work its magic.

And the difference between starting early and starting late can be enormous.

Imagine three people who all invest the same amount every month.

The only difference is when they start.

Someone who begins investing at 20 can end up with millions more dollars than someone who begins at 30 or 40.

Not because they invested more money.

Because they gave their investments more time to grow.

There’s More Than One Path to Success

One of the most surprising statistics from our conversation:

Only about 27% of college graduates work in jobs directly related to their major.

Think about that.

Most people spend four years studying something —

and then build careers doing something else entirely.

That doesn’t mean college is a mistake.

But it does mean something important:

There are many ways to build a successful life.

Some people thrive through:

college degrees

trade careers

technical training

entrepreneurship

apprenticeships

The key isn’t the path.

The key is what you do with the income you earn along the way.

The Financial Habit That Actually Builds Wealth

After working with hundreds of clients and nearly a billion dollars in investments, Mr. Pettibon shared something interesting.

The people who build wealth usually have one thing in common.

They’re not necessarily the highest earners.

They’re consistent savers.

They live within their means.

They save part of every paycheck.

And they let time do the heavy lifting.

A common rule of thumb is to invest about 15 percent of your income.

Do that consistently, and something powerful begins to happen.

Your money starts working for you. [Compare that to the idea of you working for your money — hmmmm.]

Eventually, the income from your investments begins to support your lifestyle.

That’s when you reach what everyone ultimately wants:

financial independence.

The Real Lesson

Don’t get me wrong; the purpose of this conversation isn’t to argue against college.

College is an incredible opportunity, and we here at College App Help Desk and ESSAY CURE not only went to college but also enjoy helping students to find a similar fulfilling college path.

The real lesson for our students is this:

Think about the financial consequences of your decision to purchase an education.

Ask questions like:

What will this degree cost?

What career opportunities will it open?

Are there ways to reduce the cost?

Because when you’re young, the most valuable asset you have isn’t money.

It’s time.

How you use that time can shape your financial life for decades.

Thank you, Mr. Pettibon, for sharing your time and talents with our students.

https://thecollegeinvestor.com/7868/college-worth-investment/

https://educationdata.org/average-cost-of-college

Follow-Up for Students Who Want to Build Financial Health

1. Toth Financial

A boutique wealth management and investment advisory firm headquartered in Leesburg, Virginia, that manages about $1 billion for primarily high-net-worth clients using long-term portfolio strategies. Toth Financial is an independent investment advisory firm that provides wealth management and portfolio management services to individuals, families, and institutions.

Unlike brokers who earn commissions on products, RIAs like Toth Financial typically operate under a fiduciary standard, meaning they are required to act in their clients’ best interests.

“Time is the biggest financial asset you have when you’re young.” — Todd Pettibon

2. The Psychology of Money — Morgan Housel

One of the most widely recommended finance reads for beginners.

What students learn:

Why behavior matters more than intelligence in money decisions

Why saving is more powerful than chasing high returns

Why time is the biggest wealth-building tool

Great takeaway quote:

“Wealth is what you don’t see.”

This article/book teaches students that financial success is mostly about habits.

3. The Simple Path to Wealth — JL Collins

Originally written as letters from a father to his daughter explaining money.

What students learn:

How investing in index funds works

Why avoiding debt matters

Why simplicity often beats complexity in investing

Students often appreciate how clear and practical it is.

4. Mr. Money Mustache — The Shockingly Simple Math of Early Retirement

This is one of the most famous personal finance articles online.

Key lesson:

The percentage of your income you save determines how quickly you can become financially independent.

It clearly demonstrates:

Why saving rate matters more than income

How lifestyle choices impact long-term freedom

Students often find this eye-opening.

5. The Rule of 72 Explained (Investopedia)

A simple explanation of the concepts discussed in this article.

Students can learn:

How compound growth works

Why starting early matters

How long investments take to double

Investopedia is a great beginner finance dictionary for students.

6. Consumer Financial Protection Bureau: Student Loan Basics

Very practical resource for students considering college.

Topics covered:

Understanding student loans

Interest rates

Repayment options

Avoiding excessive debt

This is particularly useful for students who are trying to understand what borrowing actually means.

7. JL Collins — Why You Should Avoid Debt

Students often assume debt is unavoidable.

This article explains:

Why consumer debt slows wealth building

Why avoiding debt early changes your financial trajectory

How small financial habits compound over time

Terms Students Should Learn:

Five financial concepts worth learning early:

Compound interest

Index fund investing

Student loan interest

Saving rate vs. income

The time value of money

Understanding just these five ideas puts a student far ahead of many adults financially.

Thank you for reading!

If you’re a student reading this, the most important thing you can do is start learning about money early.

You don’t need to become a finance expert. But understanding a few key ideas — saving, investing, compound interest, and debt — can change your financial life in ways that compound for decades.

| A guest post by

|